Project 2025 Happening NOW: Weaponizing ESG Civil Liability

Project 2025 Happening NOW: Weaponizing ESG Civil Liability

A drill down into Pleiades Strategy's 2024 Statehouse Report (Scroll to the end to listen)

I’m grateful to Pleiades Strategy for making a copy of their 2024 Statehouse Report available to me. It includes one of the most insidious, largely unreported examples of Project 2025: Happening NOW.

Before we dive into new material, here’s a review of our ESG coverage from yesterday’s newsletter:

What is ESG investing, and why should YOU care?

ESG are a set of metrics that measure how responsible a public company’s proposed investments are. In a capitalist environment that puts profits over people and the planet, ESG encourages public companies to consider more than the bottom line and shareholder return.

Companies are rated in three areas:

Environment - Does the company have policies that promote good stewardship of the environment?

Social - Does the company give back to its community? Does it treat its employees well and safeguard their health and well-being?

Governance - Does the company have ethical, transparent accounting and business practices? Does it employ a diverse leadership? Does it avoid conflicts of interest?

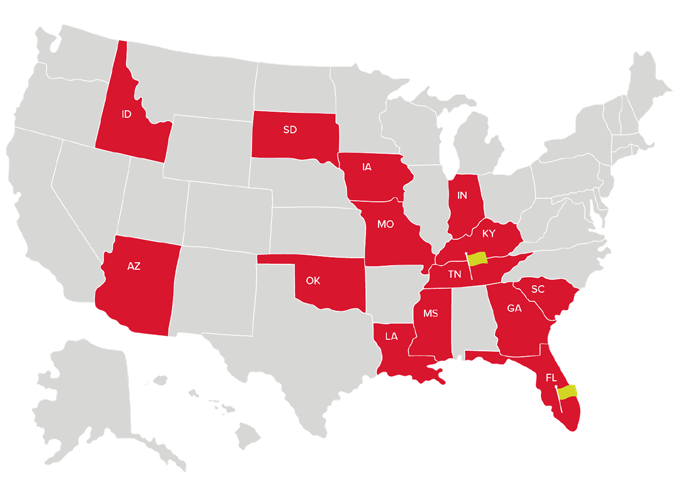

According to Pleiades Strategy’s 2024 Statehouse Report, red-state Republicans proposed 23 separate pieces of legislation to regulate private-sector alignment with ESG. Their study comparing the legislation found that the wording was nearly identical.

The “Equality in Financial Services Act” seeks to place new civil liabilities on financial institutions taking ESG factors into account…Each of these policies seeks to impose civil liability on private-sector financial institutions for incorporating a broad array of risk assessment criteria before committing to provide loans, process transactions, and offer other financial services.

SOURCE: Pleiades Strategy’s 2024 Statehouse Report by Connor Gibson, Frances Sawyer, and Jeremy Siegel

Only two states passed laws this year: Tennessee and Florida.

What does this attempt to impose civil liabilities on private-sector financial institutions mean?

These bills provide a roadmap for how a fascist Republican regime intent on revenge could punish its enemies: By weaponizing civil liability against institutions for refusing to provide financing to high-risk groups.

These bills use anti-ESG language to turn the definition of “discrimination” on its head and force financial institutions to provide services to entities involved in activity that could expose them to significant liabilities. These proposals would prevent banks from making clear-eyed risk assessments before offering services to firearms manufacturers, fossil fuel companies, and other high-risk industries. The bill language could also compel financial institutions to provide services to extremist groups, including those that promote bigoted discrimination under the guise of religious expression, and white nationalists. Based on the legislation’s backwards definition of “discrimination,” failing to provide financial services could result in civil penalties.

SOURCE: Pleiades Strategy’s 2024 Statehouse Report by Connor Gibson, Frances Sawyer, and Jeremy Siegel

These bills prohibit the use of an ESG “social credit score,” which rates how responsible a company’s proposed investments are. Essentially, use of “social credit scores” is redefined as “discrimination” subject to civil liability lawsuits.

This tranche of bills was supported by Alliance Defending Freedom, a Project 2025 contributor (not linking to them.) ADF is a Christian Nationalist group of attorneys behind a number of high-profile lawsuits in the areas of abortion, LGBTQ, removal of transgender rights, and more. Missouri Senator Josh Hawley’s wife Erin is a Vice President at ADF. The Southern Poverty Law Center lists ADF as a hate group.

How this anti-ESG tactic creates bigger, more intrusive government

According to the report, these bills give state governments several ways to fine and hassle financial institutions who use ESG “social credit scores.” Think of this tactic as the “abortion bounty hunter law” for ESGs.

After lengthy, costly court battles, financial institutions could be fined anywhere from $10,000 to $30,000 per occurrence if they are found in violation of anti-ESG law.

Financial institutions could also be subject to additional state government paperwork attesting that they are in compliance with anti-ESG law. If they are subsequently found to have violated a state’s anti-ESG law, they could be charged with perjury.

These bills also give Republican state attorneys general broad latitude to use restraining orders, making it impossible for accused financial institutions to do business.

Hate groups, gun makers, oil-and-gas industries and more high-risk businesses could see an influx of new financing that puts every American and the planet in jeopardy.

These tactics could result in a tsunami of frivolous lawsuits, hobbling our legal system.

Anti-ESG bills will destroy the environment, make workers less safe, and cause widespread business failure due to corruption. Republicans will also have the ability to weaponize civil liability laws against their enemies and run them out of business.

To read the 2024 Statehouse Report from Pleiades Strategy, hit THIS LINK and go to their website. They also have a live anti-ESG legislation tracker.

It's a circle though. Lenders will lend to anything they think is profitable, and not to things they think aren't profitable. There's a long argument to be made about whether that's good or bad, but my view is that it works best if we make good things profitable, and bad things unprofitable. Which is what we're trying to do by making companies who do bad things be liable for the externalities of that behavior, that aren't being properly accounted for. It may or may not be a crude tool, but it makes sense. (And on the flip side we can subsidize good things, whose beneficial externalities aren't being properly accounted for, such that they are more attractive investments).

The important thing Republicans are doing is flipping those incentives in the opposite direction. They will shield gun manufacturers, fossil fuel companies, and sexist and racist employers, from liability, making them more profitable (or at least less unprofitable). And then they will remove all subsidies, or even penalize, things like green energy and diversity, so that those are less profitable.

Once you do that, the lenders will follow suit. You don't need to tell them. They'll follow the money.

Alternatively, if, because of public preferences, bad things remain unprofitable, and good things become more profitable, (we can only hope), the lenders can still follow the money. They couldn't be liable for discriminating if they're just chasing profit. Unless Republicans really want to tell them they can't do THAT.

So it seems like a bit of a side show. The real action is in using the power of the state to make favored companies and interests more profitable, and unfavored ones less profitable. And they have all kinds of plans for that.

If state action outweighs consumer preference to be virtuous - and it usually does; only the wealthier can afford to factor that into their choices - that's where the real problem is.

Project 2025 Step 1: Do everything possible to prevent effective public governance at the federal, state AND local level. (that is, governance that looks at public investments through the lens of long-term resilience, the equitable distribution of the economy, and the common good)

Project 2025 Step 2: Weaponize a nefarious intrusive government to prevent private sector businesses from making similar assessments of future performance for the common good (.i.e., their customers, employees and shareholders/investors)

Project 2025 Step 3: Leverage their stranglehold on the Courts to make sure that Step 1 and Step 2 survive until there is no common wealth, only serfdom